Inverness: 01463 419 137Glasgow: 0141 440 7433

2024 – The year in review

In 2024, we were meant to experience a global slowdown. The consensus opinion was for higher inflation, rising unemployment and higher interest rates which would in turn lead to a recessionary environment. Would it be a soft or hard landing for world markets? In the end we experienced neither.

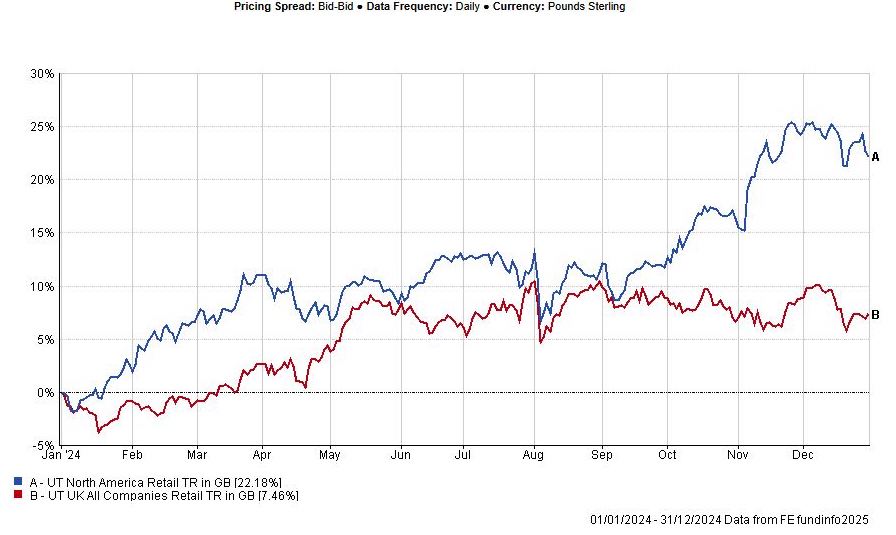

Most fascinating was the divergence across geographical regions and asset classes. The performance of the US equity markets against the UK equity markets is a prime example.

This can be attributed to a number of factors including the re-election of President Trump. The US consumer and labour markets remained incredibly resilient whilst being supported by liquidity from the Federal Reserve and fuelled by an Artificial Intelligence (AI) boom which propelled a handful of mega tech companies such as NVIDIA to the top of the global ranks.

The UK, in stark contrast, struggled to attract inward investment and the UK stock market continued to underperform. The recent Budget was not well received and, as we start 2025, we are still waiting for the promised Brexit uplift.

The rest of the world

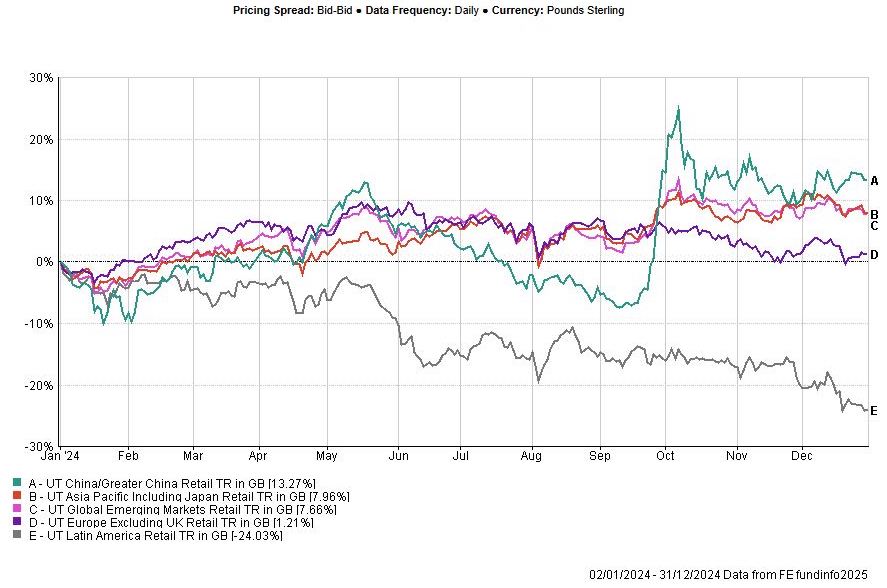

The ongoing geopolitical uncertainty posed by the ongoing war between Ukraine and Russia, as well as issues in the Middle East and parts of Asia and Latin America, polarised returns. The performance of Latin America in particular has been a surprise given its access to natural resources, industrial production and proximity to the world’s largest market in the USA. However, this has not filtered through to its domestic stock markets.

Fixed interest, energy, weather, coffee and cocoa

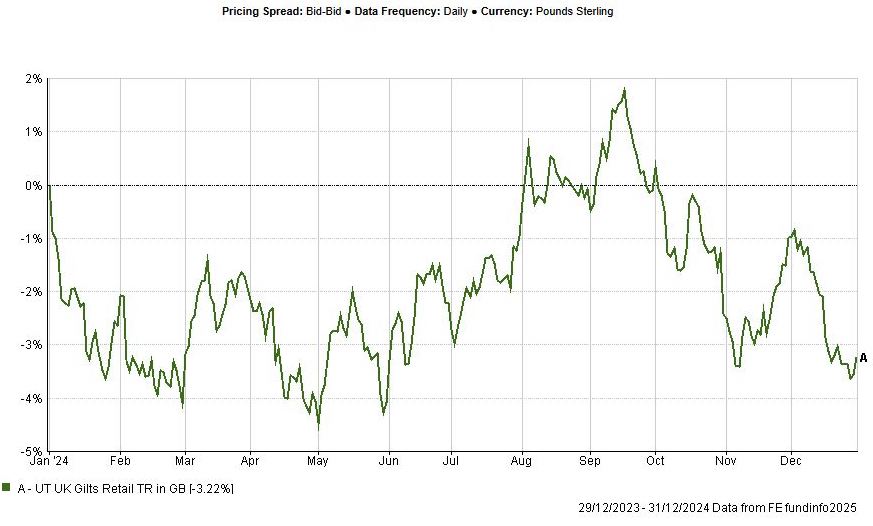

The UK, as well as the rest of the world, experienced a worrying trend where yields on fixed interest securities continued to climb to unsustainable levels, making the cost of debt repayments challenging. This is significant because the debt/bond markets are hugely important in terms of liquidity and sentiment within the overall structure. They directly affect pension funds, annuity rates and interest rate decisions and impact the majority of our clients in one way or another.

UK Government Bonds (Gilts) posted another loss for the year in what was a painful and volatile ride for our more risk averse investors. This is hot on the heels of a catastrophic 2022 and difficult 2023.

Commodity markets continued to provide opportunity but also some exceptional volatility driven by geopolitical instability. Energy prices rocked back and forth as we experienced supply issues in oil and gas markets.

The biggest swings occurred in some of our favourites - coffee and cocoa beans - where record or near record prices were reached, mainly down to extreme weather conditions in South America and Africa.

The following chart of US Cocoa Futures illustrates how prices rose from $4,000 dollars a tonne to $14,000 dollars a tonne (Source CMC Markets).

US Cocoa (Cash Futures - $)

The year of precious metals and cryptocurrencies

Precious metals had a strong year driven by inflationary fears, central bank demand, especially from Asia and India, as well as concerns for mineral rich Ukraine. Gold, silver, palladium and platinum all posted double digit returns as institutions continued to acquire physical assets.

2024 was also the year where cryptocurrencies were accepted into the mainstream and legitimised by a range of fund launches by big UK investment firms. Bitcoin reached a record high of $108,077 on 17th December, driven by President Trump’s pro crypto stance. This was an increase of more than $60,000 US from the beginning of 2024.

The UK crypto view is very different and access to cryptocurrencies within advisory firms such as ours, is still not regulated though I do believe it will happen.

Steady year for property

And last but by no means least, we look at property. Land and property prices continued to rise globally, and the UK was no exception, where it was a steady year despite the backdrop of higher rates and higher mortgage payments.

Residential prices remained resilient due to a continuing lack of supply with the annual price change for property in the UK increasing by 3.4%, according to the latest UK House Price Index provided by HM Land Registry.

Commercial property prices had a mixed year as they continued to recalibrate following the pandemic and the recent Budget. We saw the ‘Amazon effect’ with an increase in demand for warehousing and commercial units often used as regional distribution hubs. The opposite was true in city centre retail units and office blocks as more people continue to work from home post-pandemic. These properties could potentially be renovated into retail residential properties, and this is beginning to gain traction in large towns and cities. Land and farm prices dipped in the last quarter of 2024 after unpopular changes to inheritance tax rules.

Regular review is key

2024 was a solid year for returns and more consistent than recent years. However, asset allocation was critical to those returns. A high-quality, diversified and well-defined strategy would have worked well over the past 12 months, but higher risk assets produced significantly higher returns. Regular reviews of the funds and asset allocation are critical to keep the risk and performance on track.

As we start 2025, this advice is more important than ever.

Click here to read our 2025 outlook and key themes which could shape the global markets.

News Home