Inverness: 01463 419 137Glasgow: 0141 440 7433

2025 outlook

Making predictions in financial markets I have learned is most definitely a fool’s game. We prefer to look at the opportunities and threats and then consider what may be the key drivers or negatives for specific asset classes.

That being said, our job is not to time the market or to influence the risk that one takes when making an investment. Our job is to complete regular risk reviews and then allocate our clients’ assets to a broad range of investments that complement their objectives and timescales.

Opportunities and threats

TRUMP!

Whatever we think of Donald Trump as a person is largely irrelevant. He is back and we need to accept that the next four years will be driven by Trump policies. These have a huge bearing on how the rest of the world trades and operates. He has already threatened tariffs on China, Canada, Mexico and the EU. However, contrary to what you may believe, since his election win, he has been largely celebrated by equity markets and the major banks and institutions who drive market conditions. Cryptocurrency funds and a strong dollar are also indicating that they believe that monetary policy in the US will be accommodative and should bring about higher asset prices. Following his inauguration on 20th January, we have seen a steady increase in share prices although this is a small data sample, but the initial direction has been positive which contrasts with his last term.

World peace

Unlikely, but we live in hope of a de-escalation for the various conflicts currently ongoing. Even a ceasefire in Ukraine would be supportive to both bonds and equities. Trump seems determined to deliver on this and, if successful, it would certainly provide support to portfolios.

Equally, if conditions deteriorate and 2025 turns out to be dominated by further geopolitical instability then we could end up back in a 2022 type situation where risk is reduced in portfolios and more assets are held in cash deposits.

Interest rates/Central bank intervention

The consensus is that interest rates will come down across the globe. We have already seen this in the UK but to a lesser extent than the US and Europe. If we see inflation moderate, then this should provide a case for decreasing rates which in turn will help fixed interest securities and equity markets. Increases in commodity prices including energy, metals, etc could derail this, so we are not convinced this is as priced-in as everyone seems to expect.

If we see a spike in inflation and move the other way, this could be very challenging for all asset classes. This for me is still the main area to watch over the next few quarters.

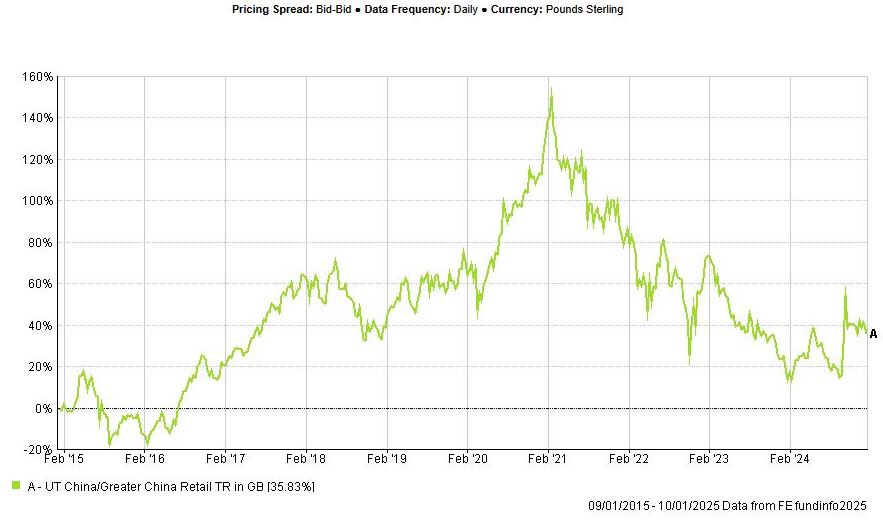

China

Chinese markets have struggled since they peaked back in February 2021. China’s post-Covid position within global trade and its more recent alignment with Russia has made this region very difficult to navigate.

However, Chinese equities may look cheap at these levels and this, coupled with the promise of massive state interventions, could make China one to watch. Trump’s relationship with Xi Jinping could also influence the overall outcome.

Proceed with caution.

Artificial Intelligence

Threat or opportunity? Potentially both. Can 2025 live up to the hype? There are many reasons to be bullish on AI, however the practical uses for this will take time to filter through and some company valuations appear to already be stretched relative to earnings. Enormous impact will arrive with AI, but we don’t believe this will be the year where this is fully optimised. Worth having some exposure to these companies going forward.

Conclusion

In conclusion, 2025 should bring opportunity but we have to be respectful of the ongoing geopolitical risks and the incoming US administration. These factors aside, it is likely that the economic backdrop to markets is positive. Global growth remains on the correct trajectory yet at the same time moderating inflation gives central banks the scope to reduce rates from current levels which is a positive for risk assets.

Only time will tell…

News Home